Unlock the secrets of blockchain technology and explore its revolutionary impact on the world.

Introduction

Blockchain technology is originally the name given to the design behind the operation of the digital currency Bitcoin. The concept of Bitcoin was introduced in 2008 when Satoshi Nakamoto wrote the paper “Bitcoin: A Peer-to-Peer Electronic Cash System.” Many believed it would have a significant impact on finance, media, government, and every industry. Some describe it as a revolution. Others believe it will be an evolution, taking many years before the practical benefits of blockchain are realized. Bitcoin’s creator never used the term of “blockchain” in his whitepaper.

Historical Context

In 1976, an article on “New Directions in Cryptography” introduced the concept of a distributed ledger. Stuart Haber and Scott Stornetta’s paper “Hot to Time-Stamp a Digital Document” introduced timestamping data. The concept of “Electronic Cash” emerged from David Chaum’s model and played a significant role in the development of Blockchain. Adam Back’s “hashcash” and Wei Dai’s “b-money” were also introduced. Satoshi Nakamoto’s 2008 paper “Bitcoin: A Peer-to-Peer Electronic Cash System” introduced the idea of a public ledger to prevent double-spending in unreplicable digital money. The first bitcoin network was launched in 2009, and Bitcoin has since become the most popular cryptocurrency. Its transparency and ability to maintain user consensus have attracted investors and led to its widespread adoption.

What is blockchain?

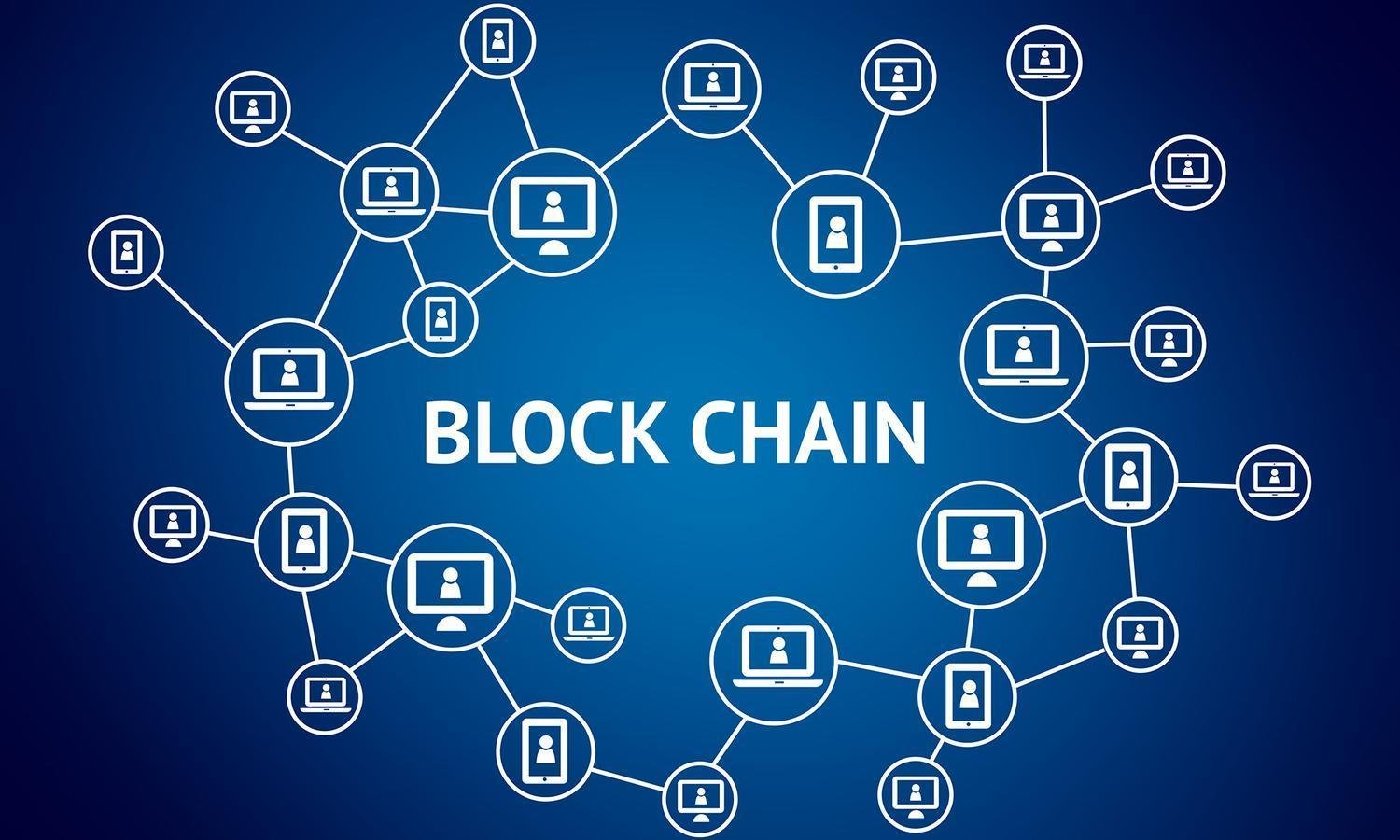

Blockchain is a distributed digital ledger that stores information of any kind. It can store information of crypto currency transactions, NFT ownership or DeFi smart contracts. Unlike any other conventional database, it is totally decentralized. Instead of a single central authority, like banks, where data is supervised by large community, where no one has access to their information, no one can go back to change or erase their information, Blockchain allows every individual on the network to access anyone’s data, which makes it impossible for a single entity to gain control of the whole network, as many identical copies of blockchain database are held on multiple computers spread out across the network. These individual computers are referred to as nodes.

How it works?

At its core, blockchain is a distributed system, so it is also essential to understand the concept of distributed system. Distributed systems are a computing paradigm where 2 or more nodes work with each other in a coordinating way in order to achieve a common objective and it is modeled in such a way that end users see it as single logical platform. A node is an individual player and all nodes are capable of sending and receiving messages to and from each other. Each node has its own memory and processor and nodes can be honest, faulty or malicious.

A node that can exhibit an arbitrary behavior is known as byzantine. This arbitrary behavior can be intentionally malicious, which is detrimental to the operation of network. The main challenge in distributed system is coordination and tolerance between nodes. Despite of the arbitrary behavior, there should be tolerance among nodes and that they should continue to work flawlessly in order to achieve the desired result.

Design of a distributed system

N4 is a byzantine

Types of Blockchain

In order to understand blockchains it is also essential to know the types of blockchain. There are 4 main types of blockchain; public blockchain, private blockchain, hybrid blockchain, and consortium blockchain.

Public Blockchain:

Public blockchains are totally decentralized, they have no access restriction. Anyone with internet connection can join, send transactions and can also participate in the process of block verification to create consensus. e.g., Bitcoin and Ethereum Blockchain.

Private Blockchain:

It is permissioned and its access is restricted by the administrator. They are efficient and faster, as they avoid complex consensus protocol.

Hybrid Blockchain:

Hybrid blockchains are a combination of both public and private blockchains. They allow for customizable access, allow for customizable access, based on which portions of centralization and decentralization are used.

Consortium Blockchain:

A consortium blockchains is a combination of public and private blockchains, where a group of organizations collaborate to create and operate the network. These permissioned blockchains, like Quorum and Hyperledger, offer greater control over access and confidentiality, making them ideal for industries like supply chain management and financial services. They are efficient, scalable, and provide greater security and reliability than private blockchains.

Pros and Cons of Blockchain

Pros

- Increased transparency: Blockchains foster trust and collaboration, as it allows everyone on the network to track transactions.

- Enhanced security: Blockchains are secure as it is impossible to alter or temper with the data because of its decentralized nature.

- Cost effective: It is low in cost because of peer- to peer transaction by effectively eliminating the need for intermediaries. Moreover, when the elimination of intermediaries is combined with enhanced efficiency and automation it could also lead to significant cost reduction.

- Traceability and auditability: Blockchain technology ensures traceability and authenticity of products, enhancing supply chain management and preventing fraud by linking each transaction to the previous one.

Cons

- Scalability problems: As the number of transaction increases and due to its nature of design, blockchain also faces scalability issues.

- High energy consumption: Mining, a process associated with public blockchains like Bitcoin, involves solving mathematical problems for validation of transaction which requires significant computational power and energy.

- Legal and regulatory challenges: decentralized nature of blockchains also gives rise to problems like dispute resolution problem because there is no central authority and uncertainty issues regarding the legal status and regulatory framework of blockchain and related technologies, as they vary greatly worldwide.

- Potential for misuse: Features of blockchain like security and privacy can also be exploited for illegal activities like money laundering and illicit trade.

- Complexity and technological understanding: The technical complexity of blockchain makes it challenging for an average person to understand and use it. This barrier hinders its mainstream adoption.